**Please note - this tutorial was written based on the 71st tax auction list. The current June 2025 list is not reflected below. The advice is still the same, but the properties detailed below have already gone through the process.

The tax auction list is finally posted, now what? In this post I'll explain how I read the list and I'll share with you the research I do for each property I'm interested in.

As a reminder, the list can be found at the Tax Department's website: https://www.hawaiipropertytax.com/taxsale.html

New this year, the county has also put the litigation guarantees online which is amazing! We will cover those later. The first step is to click on the "List, 12.18.24" link. (The list/link is only available for 30 days prior to auction and the date/link may change as they edit the list). This brings up the list. As we get closer to the auction, you'll want to check this list several times. Owners pay off their taxes owed and their properties get removed from the list. Fortunately, when this happens, the list does not get renumbered, so if you like number 21, it will always be number 21. (See #131 for an example of a "removed" property.)

Let's start with #1 on the list:

The "upset price" on this property is $6,012.54. This is the starting bid price. This is the least amount of money the county will accept to sell the property. (In years past, there would be spaghetti lots in HOVE that didn't sell even below a $2,000 upset price. When that happened, the property would be added to the end of the list and the county would try to auction it a 2nd time that day. If it still did not sell, it would be added to the list the next time around, and so on. I do not expect any of these to go unsold in this market.)

As you can see, each property shows the neighborhood, but no address. It also lists the acreage. If you decide on a minimum acreage size or if you are familiar with the neighborhoods maybe this will help you narrow down the properties you will research further. Remember, there are 120 properties on the list, so investigating all of them for potential purchase will be very time consuming.

If you are interested in Orchid Land Estates, and it meets your acreage requirements, the next step is to search it on the county tax website to look at the map. To my knowledge, this is the only way to know where the properties are. In the past, I've asked the tax office to link the list to these sites. They didn't get it done this year, but they did manage to make the litigation guarantees available online so you don't have to go review them in person, so they are making progress. Maybe next time around the TMKs will be linked. For this time though, you'll first open the county tax website search:

https://hawaiipropertytax.com/search.htmlYou'll need to put the TMK into the "search by parcel number field". Annoyingly, it needs to be in a different format than it is on the list so you cannot simply copy and past. You'll enter the TMK into the tax website without any dashes. (You can leave off the last four zeros.)

Once you've entered the TMK, the next screen has a map link:

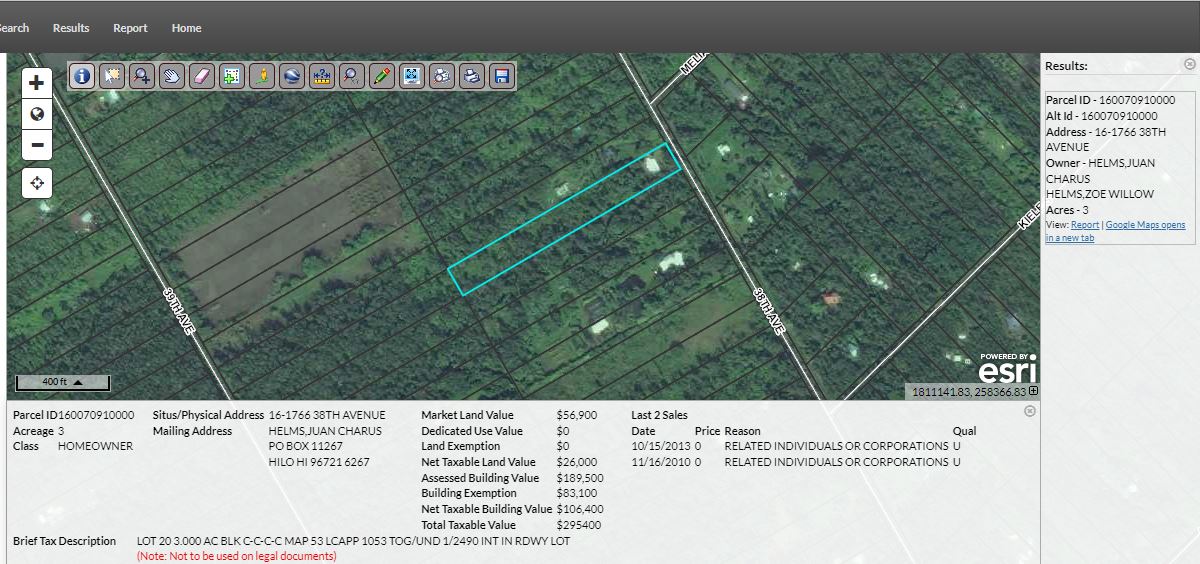

There is other info on this screen below that I revisit later if I'm interested, but my first look is the map. And, wow, what do we see on the map for the 1st item on the list? Yup, looks like a structure to me!

This is not typical. Most of the properties that end up on the tax list are raw land. Permitted houses are rarely on the list because they typically have mortgages in place, and the lenders will pay the taxes to make sure the properties don't go to auction. We will have to do more research to see if this structure is permitted and if it has a mortgage on it. But first, let's do our map research since we are on this screen.

The first thing I do is click on the parcel on either side to see who the owner is. I do not want to buy a tax sale property right next to the same owner! That would be awkward. It is very possible that someone could own two or three or more adjoining parcels, but only one of them has gone to tax auction. I usually stay away from those situations.

The other thing I do is check for the cross streets and landmarks. If you are going to do a drive-by, you'll want to know how to get there. Since most of these are vacant land, they aren't typically assigned an address. For this reason, I click on the closest parcel with a structure, to see if it has an address that I can plug into my maps. This gets me close to the parcel for a drive by. In this case, we are lucky that the parcel has an address. See top 2nd column below the map:

| Situs/Physical Address | 16-1766 38TH AVENUE |

|

I've clicked on the parcel on either side and confirmed they are not owned by the same owner as the subject parcel, and I have the address. Usually, by this step in my research, I've crossed the property off my list due to lot shape, location, obvious junk yards on the subject or neighboring properties, etc. If I'm still interested at this point, I go back to the prior screen to do a bit more research:

#1 on the list is giving us lots to look at. Most of the properties won't be this exciting. As I scrolled down on the parcel info, I get several gems of information:

First, there is a home exemption in place. This indicates that the owner occupies the property. Is this a red flag for you? It is for me! Much more research is needed now on the owner. Are they deceased? {google search their name for an obituary} Have they moved off island? {try finding them on Facebook or other social media that might tell you} Do they have a violent criminal record? {Run their name through the court website.}

Second we see the building sketch and a permit number. We used to be able to tell right way if the permit was completed, but the building department has changed this and gone to a horrible permitting system that is extremely cumbersome to use. It would take two more blogs just to explain how to find out if these permits are completed, so I won't be covering that here. Just know that you should check with the building department before assuming that a sketch on the tax site means it is permitted. Our tax department is really good at collecting property taxes and they don't care if a structure is permitted or not, they'll tax it. So, just because it has a sketch does not automatically mean it is permitted. Having a permit number also doesn't mean the permit has been completed. More research is needed.

Once I do these steps, if I am still interested in the property, my next task is to check the litigation guarantee. These are in the folder at the tax sale link: Litigation Guaranty (Title) Reports & Updates. (Link only valid 4 weeks before the auction.) They are numbered to match the list. When we open #1, we get the litigation guarantee. Litigation Guarantees are very similar to title reports. The important things I look for on this report are any liens listed in Schedule B. There will often be road maintenance liens on these properties. Sometimes PMMs (Purchase Money Mortgages which is where the prior owner acts as the lender when the property is sold, rather than a traditional mortgage lender.) and sometimes State and IRS tax liens. Again, it is very rare to have a traditional mortgage show up on one of these because the mortgagees pay the taxes to prevent the property from being sold at auction. (Schedule B always talks about mineral and water rights because in Hawaii those are always owned by the state and never the property owner. They are always listed as an exemption in Schedule B and are nothing to worry about.)

In the case of #1, we have a PMM in schedule B. This is a problem.

If you notice, it isn't even in the name of the current owner. The PMM was from 1987 and if we go back to the County Tax Website and look at the sales information, we see that the property has been transferred 3 times since 1987.

The current owner likely has no idea that the PMM is still on title. (One more reason to go through a reputable escrow company when you buy property so these types of things get cleared off before you become the owner.)

In theory, this PMM (or road maintenance liens) gets wiped out through the tax auction two ways: First, if there is an overage (anything bid above the county's upset price of $6,012.54) the additional funds go to the lien holders first, so if the PMM is still a valid lien, they can collect their funds from the county from any overage. Second, tax auctions are supposed to wipe out most liens. It isn't always easy to convince the mortgagors, road associations, or title companies of this though, so always proceed with caution and consider contacting an attorney if you're buying something with any issues listed in Schedule B of the litigation guarantee.

Beware - IRS tax liens are NOT wiped out through county tax auctions (or any other auctions to my knowledge.) There are other ways to get these removed, but consult an attorney before proceeding on anything with an IRS tax lien.

If I'm still interested at this point (so far #1 does seem very interesting) I do a drive by and I also decide on my max bid amount. As a Realtor, I have an advantage because I can more easily pull up past sales in the area to get a quick idea of current market value, but this type of data is also available on sites like Zillow. I write my max bid down and I stick to it. It amazes me how easily everyone (including myself) gets caught up in the bidding process. Most of these properties will sell very near to, and sometimes even above, market value because of the exciting auction environment.

Write down your max, stick to it.

Read my tax auction FAQ to learn more about the process on bid day. Will I see you there?